On March 6, 2024, the Securities and Exchange Commission (SEC) – by a vote of 3 to 2 – adopted long-awaited and potentially significant final rules requiring registrants to disclose certain climate-related information in their registration statements and annual reports. The final rules span nearly 900 pages and include somewhat scaled-back disclosure requirements from the rules initially proposed by the SEC in March 2022, to which the SEC received over 4,500 unique comment letters.

Disclosure Requirements

Specifically, the final rules, memorialized in a new subpart 1500 of Regulation S-K and a new Article 14 of Regulation S-X, will require registrants to disclose the following:

- Climate-related risks that have had or are reasonably likely to have a material impact on the registrant’s business strategy, results of operations, or financial condition;

- Actual and potential material impacts of any identified climate-related risks on the registrant’s strategy, business model, and outlook;

- Material expenditures incurred and material impacts on financial estimates and assumptions that directly result from any activities undertaken to mitigate or adapt to material climate-related risks;

- Activities to mitigate or adapt to a material climate-related risk;

- Oversight of climate-related risks by the board of directors and management;

- Processes for identifying, assessing and managing material climate-related risks and whether and how such processes are integrated into the registrant’s overall risk management process;

- Climate-related targets or goals, if any, that have materially affected or are reasonably likely to materially affect the registrant’s business, results of operations, or financial condition;

- Costs, expenses and losses incurred as a result of severe weather events and other natural conditions, or carbon offsets and renewable energy credits or certificates, if used as a material component of a registrant’s plan to achieve climate-related targets or goals, in each case to be disclosed in a note to the financial statements; and

- For certain large accelerated filers (LAFs) and accelerated filers (AFs):

- After a phase-in period, information about material Scope 1 greenhouse gas (GHG) emissions and/or Scope 2 GHG emissions when those emissions are material; and

- After an additional phase-in period, an assurance report at the limited assurance level, which, for a LAF, following a further phase-in period, will be at the reasonable assurance level.

- After a phase-in period, information about material Scope 1 greenhouse gas (GHG) emissions and/or Scope 2 GHG emissions when those emissions are material; and

Disclosure Presentation

Registrants will be required to file the climate-related disclosures described above in registration statements and annual reports filed with the SEC. Within those documents, the disclosures should be included in separate, appropriately captioned sections or in other appropriate sections, such as the Risk Factors, Description of Business, or Management’s Discussion and Analysis of Financial Condition and Results of Operations sections. Alternatively, registrants may incorporate such disclosures by reference from another SEC filing as long as the disclosure satisfies the electronic tagging requirements of the final rules.

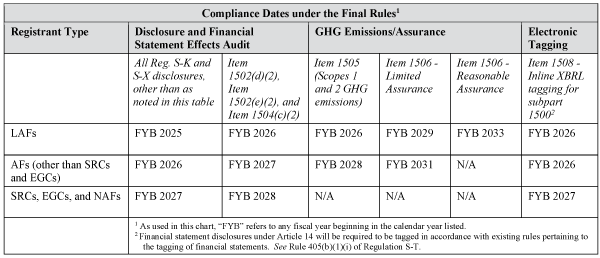

Phase-in Periods, Accommodations and Compliance Dates

As shown in the table below, all registrants will be afforded a phase-in period for complying with the new rules, the length of which is dependent on the registrant’s LAF, AF, non-accelerated filer (NAF), smaller reporting company (SRC) or emerging growth company (EGC) status. Additional accommodations include:

- Additional phase-in periods for disclosures pertaining to material expenditures, GHG emissions, the assurance requirement, and the electronic tagging requirement if the registrant is a LAF;

- A safe harbor from private liability for climate-related disclosures (excluding historical facts) pertaining to transition plans, scenario analysis, the use of an internal carbon price, and targets and goals;

- An exemption from the GHG emissions disclosure requirement for SRCs and EGCs; and

- An accommodation that allows Scope 1 and/or Scope 2 GHG emissions disclosure, if required, to be filed on a delayed basis as follows:

- For a domestic registrant, in its Form 10-Q for the second fiscal quarter in the fiscal year immediately following the year to which the GHG emissions disclosure relates;

- If a foreign private issuer, in an amendment to its annual report on Form 20-F, which shall be due no later than when such disclosure would be due for a domestic registrant; and

- If filing a registration statement, as of the most recently completed fiscal year, it should be at least 225 days prior to the date of effectiveness of the registration statement.

- For a domestic registrant, in its Form 10-Q for the second fiscal quarter in the fiscal year immediately following the year to which the GHG emissions disclosure relates;

The compliance dates for the new rules are set forth in the table below.

By way of example, a LAF with a December 31 fiscal year end will not be required to comply with the new rules (other than those pertaining to GHG emissions) until its Form 10-K for the fiscal year ending December 31, 2025, due in March 2026, with GHG emissions reporting due beginning with its Form 10-K for the fiscal year ending December 31, 2026, due in March 2027. An AF with a December 31 fiscal year end will not be required to comply with the new rules (other than those pertaining to GHG emissions) until its Form 10-K for the fiscal year ending December 31, 2026, due in March 2027, with GHG emissions reporting due beginning with its Form 10-K for the fiscal year ending December 31, 2028, due in March 2029. A SRC, EGC or NAF with a December 31 fiscal year end will not be required to comply with the new rules until its Form 10-K for the fiscal year ending December 31, 2027, due in March 2028. SRCs and EGCs are exempt from GHG emissions reporting.

Modifications to Proposed Rules

The final rules reflect certain modifications and exclusions from the proposed rules based on comments received by the SEC, including:

- Adding a materiality qualifier to certain climate-related disclosure requirements;

- Eliminating the proposed requirement to describe directors’ climate expertise;

- Eliminating the proposed requirement that all registrants describe Scope 1 and Scope 2 GHG emissions and instead limiting such requirement to LAFs and AFs and on a phased-in basis and only to the extent such emissions are material;

- Eliminating entirely the proposed requirement to describe Scope 3 GHG emissions;

- Eliminating the proposed requirement to disclose material changes to previously-filed climate-related disclosures; and

- Extending certain phase-in periods.

Legal Challenges

The final rules have already come under fire. Within hours of the SEC’s release of the final rules, a coalition of 10 Republican-led states filed a petition to block the rules with the U.S. Court of Appeals for the Eleventh Circuit. Patrick Morrisey, Attorney General for West Virginia, described the rules as “wildly in defect and illegal and unconstitutional.” Additionally, on March 13, 2024, the Sierra Club, a non-profit environmental group, and its Sierra Club Foundation, represented by Earthjustice, a non-profit public interest environmental law organization, brought suit against the SEC challenging the final rules, which in their view, with the elimination of required disclosures regarding Scope 3 GHG emissions, will yield much less information about companies’ exposure to climate-based risks than the proposed rules would have.

Next Steps

Assuming the final rules are upheld in court, registrants should consider taking the following steps in preparation for the new disclosure requirements:

- Adjust disclosure controls and procedures as necessary to ensure required climate-related information is accurately tracked and reported, including coordination with the financial reporting team to ensure compliance with financial statement disclosure requirements;

- Review board of directors and management oversight of climate-related risks, and consider whether climate-related oversight should be delegated to a committee of the board of directors and, if so, revise the charter of such committee accordingly; and

- If a LAF or AF, begin considering GHG emissions attestation providers and consider delegating oversight of such provider to a committee of the board of directors, as appropriate.

If you have any questions or would like additional information, please contact the authors or your MMM attorney.